Office address

: Budapest 1118

Budaörsi Street 48. Floor I.

Instacash: custom web development for fintech company

IT development for a digital banking marketplace

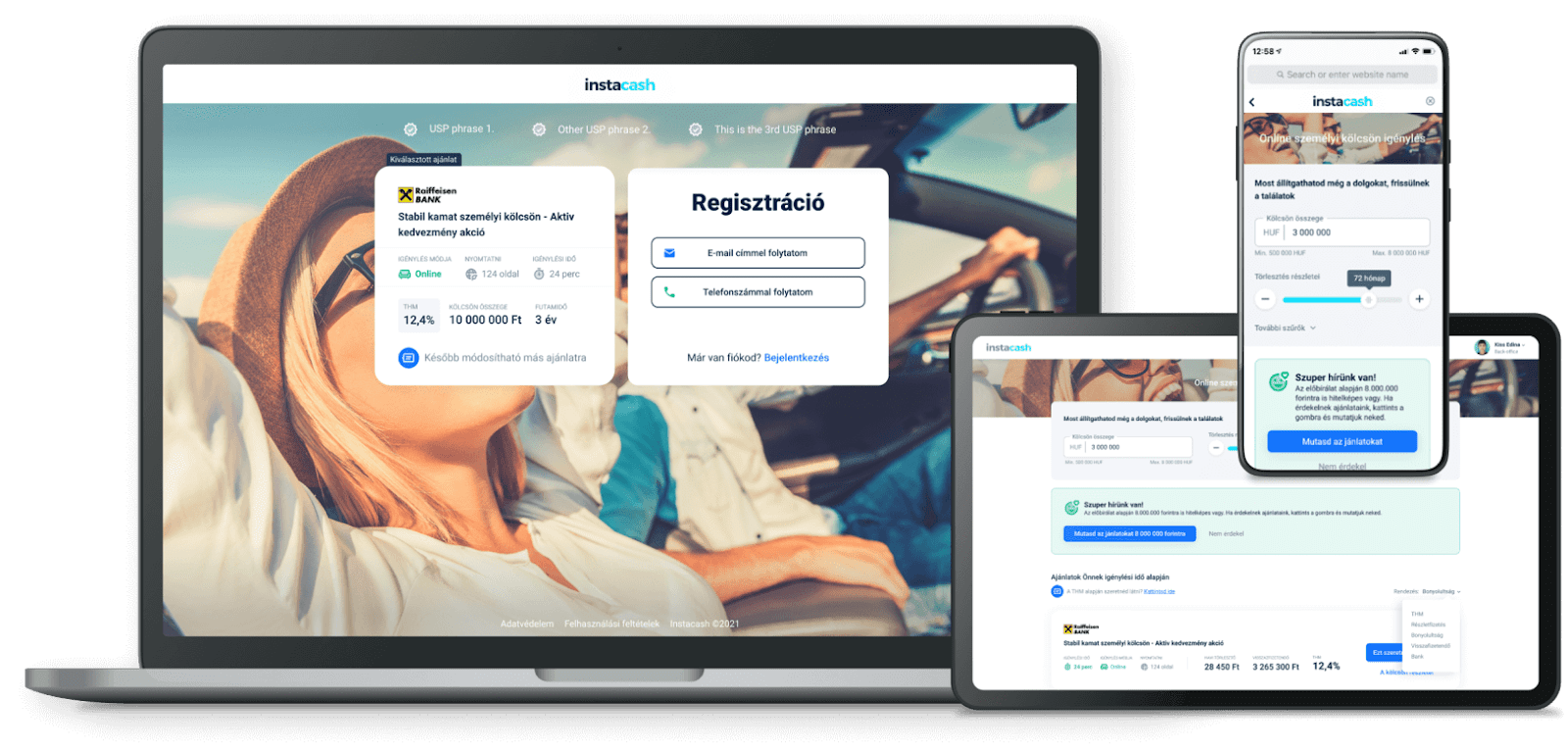

As a financial start-up, Instacash was thinking about developing an enterprise-level product that meets banking requirements, but at the same time has the flexibility of a start-up. Its aim was to build a digital banking marketplace that would allow customers to complete the entire lending process online. The custom web development required a number of modern technological solutions and an agile approach to rethink the loan application process, to find solutions for drop-off points and to incorporate security solutions that could pass an MNB audit. With the MVP (Minimal Viable Product) level version of the application, Instacash was able to go to market in just 12 weeks. Since then, the platform has been continuously fine-tuned and improved.

Instacash's own-brand delayed payment service (BNPL solution) for e-commerce retailers has been recognised by Vodafone Digital Awards 2023.

History

Instacash, a service of Hungarian fintech startup Fintrous Group, has become known as a financial aggregator. With the help of its loan calculator, those considering taking out a loan could quickly compare the offers of banks and non-bank financial service providers based on the parameters they had set. Then, with just one click, they could find themselves on the website of the financial service provider of their choice and start the personal loan process.

In response to the market demand for fast and convenient banking for customers, Instacash wanted to further develop the app, based on several examples from abroad. According to international market data, marketplace lending is already growing in the US and surrounding countries. This has also given rise to Instacash's vision to build a digital banking marketplace in the domestic fintech sector, allowing customers to complete the entire lending process online. (End-to-end online loans are loans that are processed online from application to disbursement.)

In the case of consumer loans, experience in the country shows that 70-80% of the lending process starts online, but only 20% is completed digitally. This is due to some factors, including the lack of transparency in the process and fears of time consumption. However, interest in digital credit applications is forecast to increase 2-3 times in the region, as consumer credit is the type of credit that is not complex and can do without face-to-face advice.

Although Instacash already had a business vision, it had little faith in finding a supplier that could deliver the application to a high standard in a tight 12-week timeframe. In addition to the strong professional experience, LogiNet was able to quickly get on the same wavelength with Instacash, the team understood the purpose of the product and helped the startup with sound advice and suggestions already in the needs assessment and specification phase.

Objectives and challenges

The possibility to process credit claims online and in the shortest possible time was a response to changing user needs, which were further reinforced by the pandemic.

Electronic customer identification, and thus the possibility to open an account and apply for a loan online, was already provided for in the legislation introduced in 2017 to prevent money laundering and terrorist financing. However, while online account opening has been made available by most banks, online loan application has been implemented by far fewer banks.

This was due to a lack of response to customer needs from banks. For the credit applicant, speed, transparency and simple processes are important, which is why it was important to address the perceived drop-out points in the development process.

Instacash's aim was precisely to enable individuals to access as many loan schemes as possible in an end-to-end format, and they wanted to redesign their platform to achieve this. The fintech company's vision included the creation of a partner portal where banks could assess loan applications based on the criteria they set. Customers would no longer need to visit the website of the financial institution of their choice but could apply for an "end-to-end" loan online on the Instacash platform.

To achieve this, Instacash's existing interface and processes had to be revamped, the loan application process had to be rethought and security solutions had to be built in that would pass an MNB audit.

In addition to personal loans, this approach will also be applied to merchandise loans.

Solution

1. Finding solutions to attrition points

- To put the customer in the picture at registration. Many people crumble at registration because they don't know exactly what to expect. Instacash has worked with LogiNet to make the registration process as simple as possible and provide the customer with the right information about what to expect. After just a few minutes of registration, they can see the banks' offers, take part in a digital pre-screening process, and then follow the loan application process.

- Simple registration. Efforts have been made to minimise the information requested, but at the same time, it can be modified by the bank and by type of loan, making the information requested even more flexible.

- Get a quick answer on whether the customer is eligible for credit. The customer wants to know as soon as possible whether or not he can get credit, so this is answered during the digital pre-screening process. In addition to the data entered by the customer, the application can tell this with a high degree of accuracy based on the results of previous credit applications (how banks usually respond to a given income and existing credit portfolio). In the future, the application could be complemented with a scoring & decisioning engine for decisioning, and customer rating, which would predict the expected outcome even more accurately based on algorithms from previous decisions.

- It should be clear to the customer how long the process will take. How quickly a customer can get a loan is important to them, so it was essential to see exactly where they are in the loan application process and how many steps are left. On average, it takes 20 minutes for the bank to receive your application, after which you only have to wait for the bank's decision.

- Transparent administration. With the customer profile function, the user can always see what documents he has filled in and what documents he still needs to attach. The customer is guided through the process and receives support information by SMS and, if necessary, by phone.

2. Rethinking the credit application process from a UX perspective

In parallel with the web development, the UX design of the project, the UI design, was carried out by LogiNet's UX team, 22.design. Due to the novelty of the project, it was important to break down the loan application process into more transparent steps to make it more fluid. To achieve this, they worked for almost 3 months, during which time they simultaneously developed the UX and IT, among other things:

- A thorough rethink of the business model. The first step was the Lean Canvas methodology, which was used to define the aspects of the service, its unique value proposition and whether the application was the right solution to the problem.

- Creating personas. As the loan approval process is always online, it was important for banks to be able to see as accurately as possible who the potential loan applicants are and what leads they can expect. To this end, 22.design tried to identify what goals credit applicants have, what frustrations they might face during the credit application process, and what their needs are. It was found that transparency is important to them, and although they can go through the process on their own, it is important that they feel they can always get help. Since the digital banking marketplace of Instacash is not only about the loan applicants but also about the bank employees who are responsible for the loan approval, the persona was built around similar principles. For them, it is important to be able to perform their tasks simply and conveniently, and not to take too much time to learn the new interface.

- Designing user pathways. They put a lot of emphasis on making the online interface as user-friendly as possible so that even a multi-million HUF loan application could run as smoothly as possible. A special focus was put on ensuring that this is not only considered from the user's point of view but also the admin's point of view so that the bank employee can do his job in a user-friendly online interface. User journeys were used in the design process and modified based on feedback.

- Use of frameworks. Efficiency was important throughout the development, and this was greatly helped by the fact that the recurring core elements of the UI (e.g. buttons, progress bar, date picker) were customized by 22.design using modules from a UI component library (Buefy) that can be used in a Vue.js framework. This significantly accelerated the frontend development process, as it meant that the developers did not have to start from scratch, but only had to make changes to the look and feel of the brand.

3. Partner portal: easy-to-use admin interface for Instacash and banks

In the past, Instacash's role "ended" with the customer choosing the offer that best suited him. This has changed in that the personal loan calculator is still available on the Instacash interface, but if the visitor is interested in a bank loan offer, he can start the online loan application process after registration.

Banks can access the partner portal with a reviewer's right: at a certain point in the loan application process, once the customer fills in the necessary documents and Instacash sends the lead to the bank, the financial institution will be displayed. In the admin interface, the banks "keep in touch" with the customer, where they can see their uploaded documents (e.g. proof of income, and other certificates), request a gap-fill, and validate the contract.

4. 3rd party online authentication system integration

The integration of Comnica ID into Instacash's online platform became necessary due to digital customer identification. This also includes the signing of contracts in the form of video calls, and selfie services, and eliminates the need for the customer to visit the bank branch (the customer, of course, contracts with the bank, not Instacash).

5. Ensuring further development

It was important that the application could be further developed in the future, to implement the MVP (Minimum Viable Product) approach. A quick start required compromises, as it was not possible to implement all the features and requirements in the first round. It had to be decided which features could be dropped in the first step and what would be the backlog, i.e. which improvements would be implemented after the launch.

The launch of the MVP also has the advantage for Instacash of being able to see how the service is used by customers, what needs to be changed, what needs to be improved and in what direction it should go.

6. Developments following the MVP

New services following the PSD2 directive

Following the launch of MVP, another system was integrated into the Instacash platform. Aggreg8, the first account information provider in Hungary supervised by the MNB. This will allow to provide banks reliable account information directly on the customer's bank accounts (e.g. income, existing loan repayments) instead of the customer's self-declaration.

The PSD2 has laid the foundations for open banking in the European Union, which has already triggered the development of digital financial culture in the West. In our country, few fintech companies have yet to exploit the potential of the obligation for financial institutions to give third parties access to their customer data. For Instacash, the introduction of services based on this is a development path.

Household loan end-to-end lending

A further direction for improvement could be to broaden the range of loan schemes. Currently, end-to-end lending can work for income-type loans, such as personal loans (which banks also offer), but fintech can also be incorporated for household loans.

For household loan this could be done by the webshop offering this credit option to the customer, who can then buy the higher value product of his choice on credit from his armchair. To connect the Instacash interface to the webshop engine, API development is required.

7. Technology stack

The development of LogiNet is a dockered solution designed in a modern environment, on a microservice basis. This means that the application is composed of commercially separate modules. Instacash's interface is hosted on the Amazon Web Services (AWS) cloud provider, which provides one of the most complex services. This was important because of the specificities of the financial sector. The interface was developed in Java.

Technologies and solutions applied:

- Backend: Java 11, Java 17, Spring, Spring Boot, Spring Cloud, Spring Security, Spring Data, Spring MVC, Spring Integration, JPA, Hibernate, QueryDSL, Lombok, RabbitMQ, RESTful, OpenAPI, JSON, JWT, Maven, Gradle, Docker

- Devops: AWS, Kubernet

- Digital product design: UI design, lean canvas, persona creation, user journey map, VueJS, Buefy

8. Customer service has an important role

Online credit management requires more attention to customer management tasks. In an online loan application process, there may be several points where an individual may become unsure, so it is a great help if the administrator can "engage" the borrower in the application process through chat, texting or phone calls.

Results

The development was completed in almost three months, using agile methods and modern technology. Due to the short deadline, decisions had to be made on several out-of-the-box solutions, i.e. which features could be dropped in the first step and what should be the backlog, i.e. the tasks left for after the launch.

Here are the results in brief:

- Hundreds of features included

- 200M+ disbursed loan personal loan

- New features: selfie identification (eKYC - Comnica), PSD2

- Solution validated by several leading banks

- Easy extensibility, upgradability

- 10x increase in 2021 revenue (y/y), 3x increase in 2022 revenue forecast

- Positive feedback highlighted the speed of processing (some people completed the loan application process while waiting in their cars), the quality of customer service and transparency.

- Successful MNB audit. A financial system was produced that met the requirements in all aspects, including the development and operation policies, the development team, and the application. It also passed the penetration test conducted by an external service provider to check the possibility of hacker attacks without any problems.

Thinking about custom web development, fintech, healthtech startup digital solutions? As a web development company, we offer a full range of IT services, from design to implementation, operation and support. Our client base ranges from SMEs to large corporations, covering many industries (from telecoms to fintech and healthtech to e-commerce), we outsource for several companies. We can help you develop software solutions tailored to your company's needs. Contact us for a free consultation!

Loginet Systems kft.

-

-

HQ address : Budapest 1221

Vihar St. 5D. bdg. 4. floor 15. -

-

-